For many Asian economies, this creates additional challenges. Because oil is priced in dollars, a stronger dollar can increase the domestic currency cost of energy imports. At the same time, tighter global financial conditions—including through widening sovereign spreads—can raise borrowing costs and reduce capital inflows, particularly in more vulnerable emerging markets.

Not all economies in Asia face the same level of risk. Large energy-importing economies—including the People’s Republic of China (PRC), India, Japan, and the Republic of Korea—are particularly exposed because of their heavy dependence on imported crude oil. The PRC alone imports around 11 million barrels of oil per day, making it the world’s largest oil importer.

Some smaller economies dependent on fossil fuel imports may be even more vulnerable because of relatively high macroeconomic sensitivity. Countries such as Pakistan, Sri Lanka, and Thailand rely heavily on imported energy, and rising oil prices can quickly translate into higher inflation and pressure on current accounts and exchange rates.

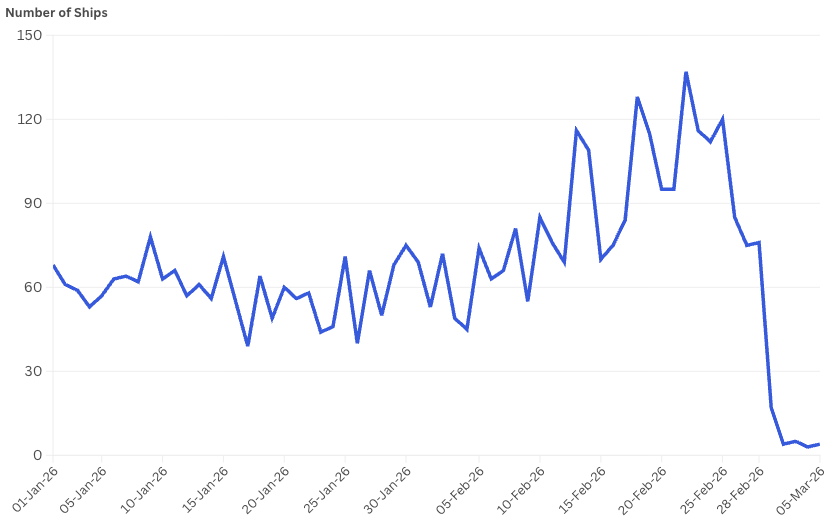

Exposure alone does not determine vulnerability. The availability of emergency oil stocks, commonly referred to as Strategic Petroleum Reserves, materially affects how long economies can cushion an energy supply disruption. Japan, the Republic of Korea, and the PRC have several months of reserves, while India’s reserves are somewhat less. Tourism-dependent economies such as Maldives, Sri Lanka, Thailand, and Pacific economies may face additional risks if aviation disruptions persist. Airspace closures across parts of the Middle East have already forced airlines to reroute flights, potentially affecting tourism flows and air cargo shipments.

The overall economic impact will depend on how the conflict evolves. If tensions remain contained and major shipping routes stay open, the economic effects may be limited mainly to higher energy prices and increased market volatility.

However, a more severe escalation—particularly one involving prolonged disruptions to the Strait of Hormuz—could have more significant consequences. Sustained disruptions could push oil prices much higher, weaken global trade, and slow economic growth.

The policy response should focus on stabilization rather than suppressing price signals. Shielding consumers from higher domestic energy costs through price controls or subsidies could distort market incentives and undermine the efficient allocation of resources. To protect vulnerable groups, targeted support is needed.

Central banks should prioritize reducing excessive swings in exchange rates and liquidity provision before tightening monetary policy aggressively, especially where inflationary pressures originate externally. Premature or excessive policy tightening could suppress growth and exacerbate financial volatility.

Governments can also play a role by monitoring early warning signs—such as shipping costs, aviation disruptions, and financial market volatility—that may signal deeper economic stress.

Economies in Asia and the Pacific have shown remarkable resilience to global shocks in recent years. To better withstand new challenges caused by the current conflict in the Middle East, it will be critical to strengthen energy security, diversify supply chains, and maintain sound macroeconomic policies.