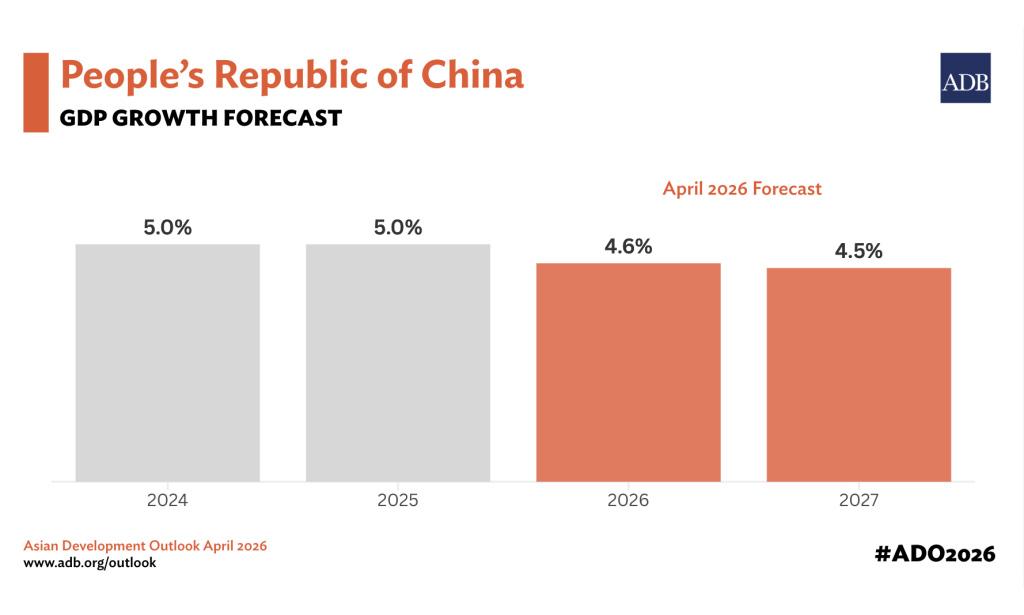

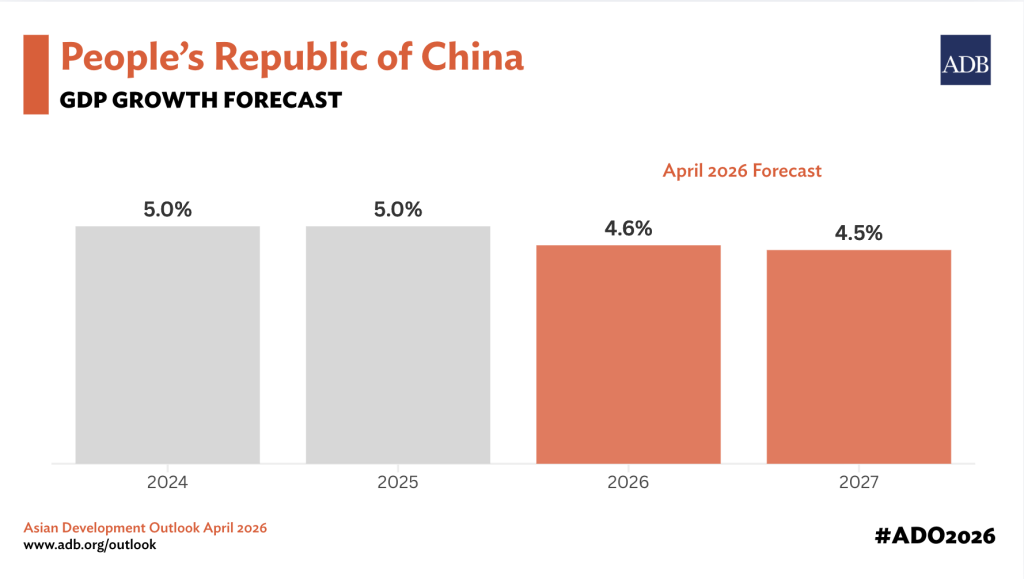

MANILA, PHILIPPINES (10 April 2026) — Economic growth in the People’s Republic of China (PRC) is projected to moderate to 4.6% in 2026 and 4.5% in 2027, while inflation is expected to edge up amid higher global energy prices and external uncertainty, according to the Asian Development Outlook (ADO) April 2026, released today by the Asian Development Bank (ADB).

The PRC economy expanded by 5.0% in 2025, supported by strong exports and resilient industrial activity. However, subdued household consumption and a prolonged downturn in the property sector are expected to weigh on growth. Exports and government investment in strategic and high-tech sectors are projected to remain key near-term growth drivers, partly offsetting weak domestic consumption and uncertainty in external demand due to the conflict in the Middle East.

“Exports, investment in advanced manufacturing and services are expected to continue supporting growth, but reviving household consumption will be critical for sustaining momentum,” said ADB Country Director for the PRC Asif S. Cheema. “Policies that strengthen income prospects, social protection, and consumer confidence will play an important role in supporting domestic consumption. We also need to continue monitoring the macroeconomic implications of the Middle East conflict.”

Inflation is forecast to rise to 0.6% in 2026 and 1.0% in 2027, from 0.0% in 2025, reflecting rising food costs and other factors, such as anti-involution efforts and higher global energy prices driven by the Middle East conflict.

Fiscal policy is expected to remain supportive, with greater emphasis on social spending. Monetary policy is also projected to stay accommodative to support growth, particularly in services consumption and strategic sectors.

Downside risks to the outlook have increased. If global energy prices remain elevated and supply chain disruptions persist, this could dent growth through higher energy costs, supply chain and trade disruptions, tighter financial conditions, and weaker investment and consumption sentiment. Additional upward pressures on production costs and a worsened business environment stemming from a prolonged Middle East conflict could weigh on corporate profitability, employment, and private investment and consumption sentiment.

ADB is a leading multilateral development bank supporting sustainable, inclusive, and resilient growth across Asia and the Pacific. Working with its members and partners to solve complex challenges together, ADB harnesses innovative financial tools and strategic partnerships to transform lives, build quality infrastructure, and safeguard our planet. Founded in 1966, ADB is owned by 69 members—50 from the region.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}